Could claims that economic growth can persist forever and ever and global warming is not an obstacle actually be delusional? Steve Keen offers evidence.

Daniel Susskind’s book “Growth: A Reckoning” is far more remarkable for what it omits than for what it contains, and for the factors to which it pays scant attention, more so than those it emphasises.

This is a book on economic growth, published in April of 2024, which contains only one reference to Global Warming—and even then, without the adjective “Global” on page 99. “Fossil fuels” make a first, brief appearance on page 100, then disappear for 135 pages, after which they return a few times between 100 and 80 pages from the book’s end. The word “energy” first appears (as something other than the title of a body or person) on page 162 (almost 60% of the way through the book), and not as a possible explanation of the phenomenon the book purports to both explain and champion—economic growth—but in a criticism of the degrowth movement.

These omissions could be seen as foibles of the author, were it not for the enthusiastic endorsements the book received from such economic luminaries as Larry Summers, Andy Haldane, Daron Acemoglu and Diane Coyle. The factors the author ignores therefore reflect not merely the author’s foibles, but those of the discipline of economics itself—or rather, of the “Neoclassical” school of economic thought that has dominated the profession ever since the 1970s. The reasons why these issues are omitted or trivialised illustrate why it is extremely dangerous for humanity to take the advice of mainstream economists on the question the book purports to address: what caused economic growth to commence in the 1700s, and whether that growth can and should be sustained in future.

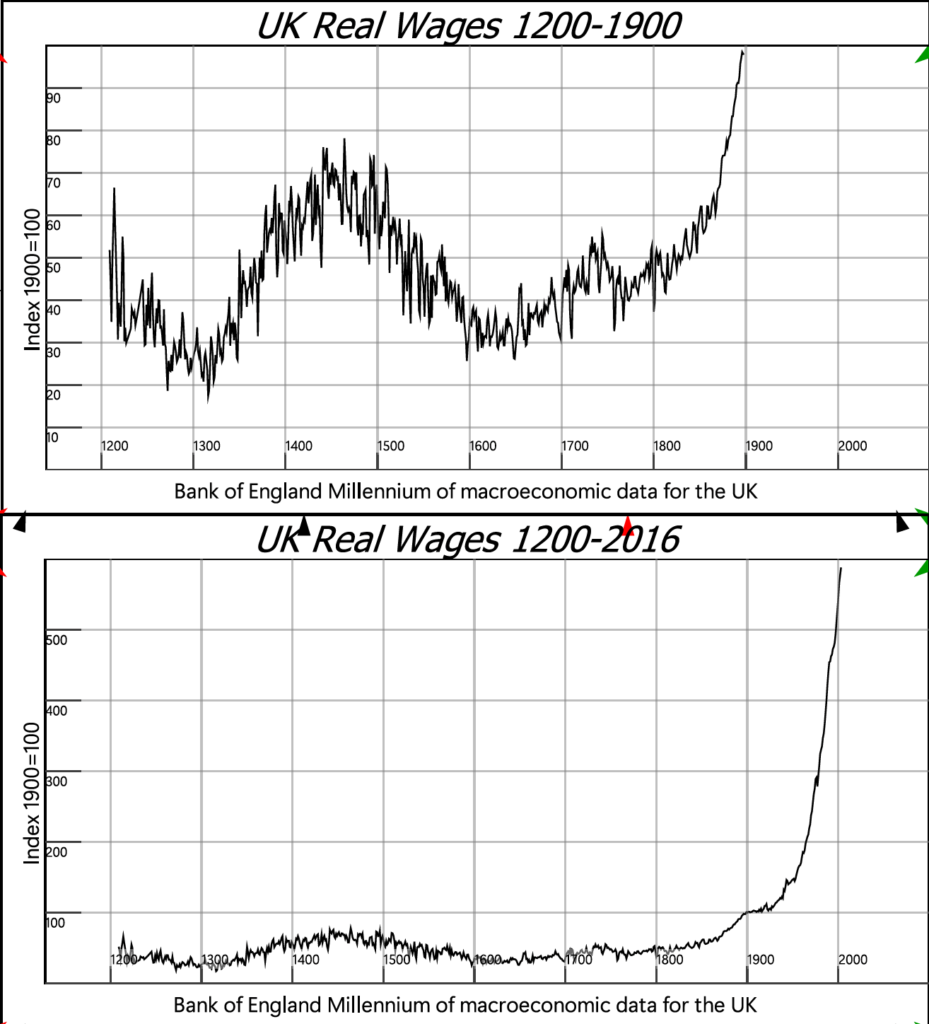

The book opens with a significant statistic: the dramatic increase in the real income of the majority of the UK’s population which began in the early 1800s. As Susskind puts it:

“Six centuries rich in revolutionary moments – the arrival of the printing press in the fifteenth century and the attendant explosion in literacy, the English Reformation in the sixteenth century and a violent religious schism, the Glorious Revolution in the seventeenth century and a new conception of the state – yet economic life was essentially unchanged. According to Figure 1,an Englishman’s living standard, measured by his real wages, was no better in 1809 than back in 1209.” (p. 4)

My Figure 1 is, like Susskind’s, sourced from the Bank of England’s excellent Millenium of Macroeconomic Data project, and it shows that real wages fluctuated at between 1/5th and 2/3rds of 1900 levels for six centuries, before rising by more than tenfold since the Industrial Revolution.

This is an incredibly significant event in human history, which deserves a serious explanation. What Susskind provides instead is an explanation that is both trivial, and consistent with Neoclassical economic theory.

The four pillars of Susskind’s explanation for economic growth are (1) the Neoclassical concept of diminishing returns (also called “diminishing marginal productivity”); (2) Robert Solow’s economic growth model; (3) Paul Romer’s model of endogenous technical change; and (4) Joel Mokyr’s argument that a culture of growth in Europe enabled the Industrial revolution to commence there in the 18th century, and not elsewhere or at some other time.

Diminishing returns is the hypothesis that, as more and more variable inputs are added to a production process with fixed inputs, total output will rise, but at a diminishing rate:

“Picture a factory where workers use machines to produce some output. As we have seen, if you increase the number of workers and do nothing else, you will hit diminishing returns: perhaps the machines get overcrowded or people get in one another’s way, and new workers will start to add less than those that came before.” (p. 38, emphasis added).

Diminishing returns is Susskind’s explanation for what he calls “the ‘Long Stagnation’, a one-hundred-thousand-year stretch in which very little changed in the living standards of human beings at all” (p. 4, emphasis added). Its 600-year-long tail end is shown in the top plot in Figure 1.

Solow’s economic growth model puts diminishing marginal productivity in the mathematical form of a “production function”, augmented by a technology factor that economists normally call “Total Factor Productivity” (TFP). Labour and Capital, the two inputs to Solow’s production function, are subject to diminishing returns, but TFP is not. Therefore, prosperity can rise indefinitely: technological progress, if sustained, meant that those workers or machines would also become more productive as time went on. The result was a clash between two fundamental forces: the harmful force of diminishing returns and the countervailing helpful force of technological progress… when capital was accumulated at the perfect rate, diminishing returns were offset by technological progress, and the economy was suspended in a state of perpetually rising prosperity. (pp. 33-34)

Susskind portrays Romer’s model of endogenous technical change as the explanation for rising productivity from technology. Technology embodies ideas, and, as intangible things, ideas are “non-rival… ideas can be used and reused without limit and without leaving fewer ideas for others”. (p. 38)

This explanation, however, applies for all time, leaving unanswered the question of why growth took off during the Industrial revolution:

“what exactly happened during the Industrial Revolution – people surely had ideas before then, so why did growth only take off at that point?” (p. 45).

Here, Susskind introduces Mokyr’s argument that there was:

“a profound change in culture during the eighteenth century… people were no longer content to understand the world for the sake of intellectual satisfaction or to make abstruse philosophical observations, as in the Scientific Revolution or the Enlightenment, but wanted to use it in the real world ‘to improve mankind’s condition”. (pp. 50-51).

The glaring omission in this explanation of growth and prosperity by a 21st-century Neoclassical economist is best illustrated by comparing it to the explanation of the same phenomena given by one of the founders of Neoclassical economics in the 19th-century, William Stanley Jevons. Jevons began his book The Coal Question, which was first published in 1865, with the statement that:

“DAY by day it becomes more evident that the Coal we happily possess in excellent quality and abundance is the mainspring of modern material civilisation. As the source of fire, it is the source at once of mechanical motion and of chemical change. Accordingly, it is the chief agent in almost every improvement or discovery in the arts which the present age brings forth.” (Jevons 1866, p. 1. Emphasis added).

Jevons thus credited, not ideas in general, but energy, and coal in particular, for the growth ignited by the Industrial Revolution. Ideas were of course critical to harnessing this energy—ideas like Watt’s idea of a separate condenser to dramatically improve the efficiency of Newcomen’s steam engine. But what clearly distinguished the ideas of the Industrial Revolution from the ideas of the Scientific Revolution was not the culture in which they occurred—though culture does matter—but the energy they enabled the UK to harness from coal. And these intangible ideas did not matter until they were turned into very tangible machines embodying them, such as Newcomen’s steam engine in 1712, and Watt’s dramatically more efficient engine in 1776.

The statistics strongly support Jevons’ perspective that energy—and specifically, energy from coal—caused rising living standards in the UK (see Figure 2). Coal, and not a hypothesised change in culture, propelled the rise in living standards that Susskind attributes to intangible ideas.

That trend continues today, with energy in general at the global level. Though some individual countries display an apparent “decoupling” of Gross Domestic Product (GDP) from energy, Gross World Product (GWP) and energy are even more tightly coupled than GDP and energy were in the UK during the Industrial Revolution: GWP has risen because energy consumption has risen. The correlation between GWP and Energy is 0.995, and while this high figure is in part because both GWP and Energy are generally increasing, the correlation of change in energy to change in GWP is still a staggering 0.83—see Figure 3. To a first approximation, GWP is energy, converted from the raw forms which we find in Nature, into forms that are useful for human consumption.

How could the role of energy in production be so obvious to Jevons 160 years ago, and so obvious in the data, and yet be ignored by Susskind—and modern Neoclassicals in general, given his prestigious endorsers—today? The answer lies in Susskind’s first two pillars: the hypothesis of diminishing returns, and Solow’s growth model. This hypothesis, and the development of Solow’s growth model from it, has ultimately blinded Neoclassical economists to the critical role of energy in production.

Solow’s growth model was based on the first-ever “production function”, which was created by Cobb and Douglas in 1928. The “Cobb-Douglas Production Function” (CDPF) describes output as a function of Labour and Capital inputs, where these inputs were raised by powers that summed to one. This was done to ensure “constant returns to scale”: doubling all inputs, given no change in technology, would double production. It also necessarily generated diminishing returns, which, as Susskind declares, is treated as a “Law” by Neoclassical economics:

“In economics, this phenomenon is thought to be so pervasive in real life, and so plausible a foundation for theoretical models, that it has been elevated in status to the ‘Law of Diminishing Returns”. (p. 21)

There was some initial opposition to the CDPF, but because it was so compatible with both the ‘Law of Diminishing Returns’, and the Neoclassical theory of income distribution, over time, it became the dominant way that Neoclassical economists modelled production.

Today, mainstream economists think of production as a function of the inputs of Labour and Capital—and they have, therefore, forgotten about energy.

For example, the economist William Nordhaus, who was awarded the Nobel Prize in economics for his work on climate change, said in 1991 that:

“for the bulk of the economy—manufacturing, mining, utilities, finance, trade, and most service industries—it is difficult to find major direct impacts of the projected climate changes over the next 50 to 75 years.”

This is absurd, because all of these industries require energy to operate. Since global warming is caused by burning fossil fuels to generate energy, all of them will be affected by climate change. And yet economists cannot see this, because their preferred model of production pretends that output can be produced by a combination of “technology” and Labour and Capital, with no inputs from the natural world.

This is nonsense: without inputs from the natural world, and especially inputs of energy, nothing can be produced. Nor can Labour or Capital function without energy—as the Cobb-Douglas Production Model pretends. Instead, as my co-authors and I put it in “A Note on the Role of Energy in Production”:

“labour without energy is a corpse, while capital without energy is a sculpture.”

Therefore, neither Labour nor Capital can produce anything without energy inputs. But Neoclassical economists in general cannot see this, because energy is not an input to their dominant model of production.

Susskind’s opinions about the viability of continued economic growth show the consequences of ignoring the role of energy in maintaining it, as well as the effect of believing that intangible things—ideas—explain growth, and not energy. Of course, ideas matter, but in the real world, ideas only lead to rising living standards if they enable an increase in energy consumption per head.

The real world also imposes limitations upon the use of energy within the Earth’s biosphere, about which Susskind is not so much ignorant as dismissive—again, because he epitomises the ignorance that Neoclassical economists have about energy. For example, he acknowledges part of the argument for degrowth—that “that our current growth path is destroying the planet” (p. 155). This aspect of degrowth, he concedes, is “relatively unimpeachable”:

“Indeed, if anything … degrowthers probably understate their case in terms of the total damage done to our lives: the undesirable dimension of growth is not simply that it is climate-destroying, as they emphasize, but also that it is inequality-creating, work-threatening, politics-undermining and community-disrupting. So far, so obvious.” (p. 156)

But he rejects the proposition that “that ‘infinite growth is not possible on a finite planet’. “(p. 156). Citing Larry Summers and Nobel Prize winner Paul Romer in support—which shows how his views are pervasive within the economics discipline— Susskind states the opposite: “it is possible to have infinite growth on a finite planet”. (p. 156)

His logic is an extreme version of the argument that a move towards a service-based economy will “decouple” GDP from physical inputs:

“the idea of a ‘finite planet’ is rooted in an old-fashioned view of economic activity. It pictures the economy as a material world, a place where tangible stuff is combined to produce more tangible stuff … it’s true that in a solely material world there are obvious physical limits on economic activity: only so many acres of land that can be farmed, only so much raw material for production. But contemporary service-based economic life is far more weightless than the old world of farms and factories.” (pp. 156-157)

The bottom-left plot in Figure 3 gives the lie to this fantasy of a virtual world that will enable infinite growth. Yes, the ratio of GDP to energy has risen over time—from $3,500 per tonne of oil in 1970, to $6,000 in 2020. But the trend is linear, not exponential, and far too gradual to support Susskind’s empirically vacuous assertions.

The service-based economy that Susskind sees as enabling growth forever also depends upon energy. Virtual worlds only exist while electricity is supplied to data centres and while air conditioning and water-cooling systems remove their waste heat. In fact, elements of the virtual world—from Bitcoin to AI—are already making dramatic demands upon electricity consumption.

There is much else that I could criticise in this book. But the real problem is not this book itself, but the fact that the economics discipline in general is as naïve about the biophysical underpinnings of our current economic prosperity as is Susskind. This would not matter if economists were merely a fringe sect, like Flat-Earthers. But they are in fact front and centre in the formation of climate policy, and their advice to politicians is to not worry. For example, the economics chapter of the 2014 IPCC Report declared in its Executive Summary that:

“For most economic sectors, the impact of climate change will be small relative to the impacts of other drivers (medium evidence, high agreement). Changes in population, age, income, technology, relative prices, lifestyle, regulation, governance, and many other aspects of socioeconomic development will have an impact on the supply and demand of economic goods and services that is large relative to the impact of climate change.”

This dangerously misinformed analysis is as important as the self-serving lobbying by fossil fuel companies in explaining why humanity has done so little to address the challenge of global warming. The one positive benefit of Susskind’s book is that it illustrates why economists have fallen for the delusion of imagining that infinite growth is possible on a finite planet.